.png)

TL;DR:

- Many Romanian companies mistakenly treat sustainability KPIs like financial metrics, risking non-compliance under CSRD.

- CSRD requires KPIs to be traceable, methodology-defined, and linked to specific ESRS data points for auditability and comparability.

Many Romanian companies assume sustainability KPIs work like financial ones: pick a metric, track it consistently, and you’re done. That assumption can cost you dearly under CSRD. The ESRS disclosure requirements demand that every KPI trace directly to a specific datapoint, carry a defined methodology, and disclose its estimation basis. For manufacturing and construction companies in Romania, where Scope 3 data is scarce and value chains are complex, getting this right is both a compliance obligation and a genuine operational opportunity.

Table of Contents

- What makes a sustainability KPI fit for CSRD?

- Environmental KPIs: Climate, pollution, water, and circularity

- Managing value-chain data gaps and estimation

- Benchmarking, assurance, and KPI simplification

- Fresh perspective: Why true KPI usefulness depends on mapping, not measuring

- Solutions for CSRD-ready sustainability KPIs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| ESRS-aligned KPI mapping | Every sustainability KPI should be mapped directly to an ESRS disclosure requirement and backed by a transparent methodology. |

| Sector-driven environmental focus | Energy consumption, GHG emissions, pollution, water, and circularity are the primary metrics for manufacturing and construction under ESRS. |

| Proxy data management | Handling indirect value-chain metrics requires disclosure of estimation sources, accuracy, and improvement actions. |

| Benchmarking with caution | Comparisons across sectors must use equivalent ESRS indicators or clearly labeled management metrics to avoid misleading results. |

| ESRS simplification | Recent ESRS changes reduced reporting complexity, with a 61% cut in mandatory datapoints while retaining assurance standards. |

What makes a sustainability KPI fit for CSRD?

With the regulatory landscape established, let’s break down what truly sets CSRD-oriented sustainability KPIs apart.

Most companies start with what they can measure: energy bills, fuel invoices, waste tonnage. That’s a reasonable starting point, but CSRD asks for something more structured. Your KPIs must map to ESRS disclosure requirements, meaning every number in your sustainability statement should be traceable to a specific ESRS datapoint with a clear audit trail.

Think of it as building a disclosure-to-data map. For each ESRS requirement, you identify the exact KPI, the data source, the calculation boundary, and the methodology used. This is not bureaucracy for its own sake. It’s the architecture that makes your report auditable and your KPIs genuinely comparable year over year.

Here is a practical breakdown of what CSRD-fit KPIs require across key dimensions:

| KPI dimension | What CSRD requires | Common gap |

|---|---|---|

| Methodology | Defined calculation standard (e.g., GHG Protocol) | Ad hoc calculation with no documented basis |

| Boundary | Organizational and operational scope stated | Unclear which entities or activities are included |

| Estimation | Sources, proxies, and accuracy level disclosed | Numbers reported without provenance |

| Improvement plan | Year-over-year accuracy improvement documented | Static data quality with no roadmap |

| ESRS traceability | Linked to a specific ESRS datapoint code | Reported in isolation from regulatory structure |

A few principles that follow from this structure:

- Define before you measure. The methodology and boundary must be decided before data collection begins, not after.

- Document estimation openly. If 40% of your Scope 3 data relies on sector-average emission factors, say so. ESRS expects this transparency.

- Track quality over time. Auditors and assurance providers will look for year-on-year improvement in data coverage and accuracy. A static data quality is a red flag.

Pro Tip: Build your KPI register as a living document in a shared system, not a spreadsheet that gets rebuilt every year. Each entry should list the ESRS code, data source, methodology version, and any known gaps. This makes assurance preparation dramatically faster.

For more background on navigating the regulatory framework, the CSRD compliance guidance and assessing sustainability KPIs resources lay out the practical steps in detail. You can also find a deeper treatment of disclosure obligations in the sustainability statements compliance guide.

Environmental KPIs: Climate, pollution, water, and circularity

Now that we understand CSRD KPI requirements, let’s focus on which environmental metrics matter most in your sector.

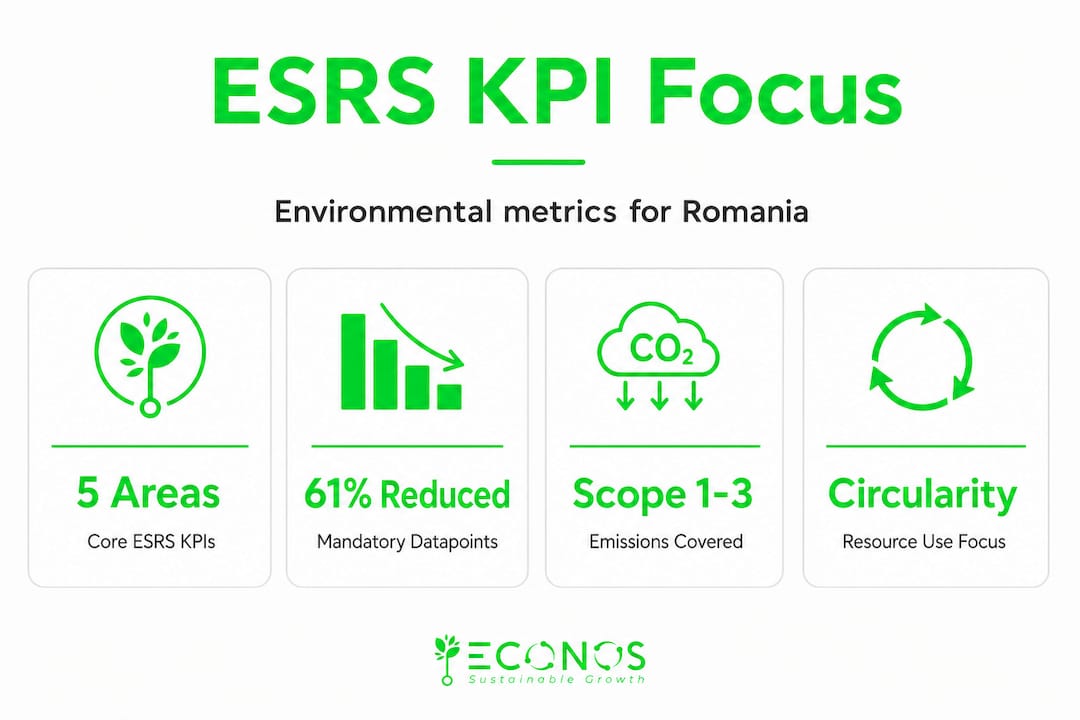

The core environmental KPIs under ESRS cover five primary areas: climate and energy, air pollution, water, biodiversity, and circularity. For manufacturing and construction in Romania, the most material ones tend to cluster around climate, pollution, water use, and waste/resource flows.

Here is how the main environmental KPI groupings compare in terms of reporting focus and data sources:

| ESRS topic | Primary KPI | Typical data source | Sector relevance |

|---|---|---|---|

| Climate (E1) | Total GHG emissions (Scope 1, 2, 3) | Fuel records, energy bills, spend data | High for manufacturing and construction |

| Energy | Total energy consumption, energy intensity | Utility meters, invoices | High across sectors |

| Pollution (E2) | Emissions to air, water, soil | Environmental permits, monitoring reports | High for manufacturing |

| Water (E3) | Water withdrawal, consumption, discharge | Water meters, site records | Medium to high depending on process |

| Circularity (E5) | Waste generated, recycling rate, material input | Waste manifests, procurement records | High for construction |

The numbered approach to Scope emissions matters here. Let’s be specific:

-

Scope 1 covers direct emissions from your own facilities and vehicles. Data comes from fuel consumption records, on-site process measurements, and refrigerant logs. Most Romanian manufacturers can collect this with reasonable accuracy today.

-

Scope 2 covers purchased electricity and heat. Location-based reporting uses the Romanian grid emission factor; market-based reporting uses supplier-specific factors or residual mix. The choice of method must be stated explicitly.

-

Scope 3 covers all indirect emissions across the value chain, from raw material extraction upstream to product use and end-of-life downstream. This is where data gaps are largest. Procurement spend, supplier questionnaires, and logistics data are common starting points.

One often-overlooked point for construction companies: the embodied carbon in materials (concrete, steel, insulation) can account for over 50% of a building’s lifetime emissions. ESRS E1 requires you to address this in your value chain reporting, even if you rely on generic emission factors from databases like ecoinvent or the ICE database for now.

For a practical workflow tailored to your industry, the ESG workflow for manufacturers guide walks through data collection sequencing, while the ESRS compliance guide Romania provides country-specific context for local regulatory alignment.

Managing value-chain data gaps and estimation

A major challenge is obtaining value-chain data. Here’s how to handle gaps and maintain clear reporting.

Value-chain data gaps are not a failure of effort. They are a structural feature of first-generation CSRD reporting. Suppliers are not yet required to share ESRS-grade data, procurement systems were not designed to capture emission factors, and logistics data is fragmented across carriers. Admitting this is not weakness. It is what ESRS actually expects from you.

The ESRS General Disclosures guidance requires you to disclose the sources of your metrics, the basis for any estimation, the accuracy or confidence level, and your plan to improve data quality over time. This is a four-part obligation, and most companies only address the first part.

Practical approaches for managing gaps:

- Spend-based proxies for Scope 3. Use financial data and sector-average emission intensity factors (from databases like Exiobase or USEEIO) to estimate upstream emissions when supplier-specific data is unavailable. Document which categories you estimated this way and at what confidence level.

- Industry benchmarks for pollution and water. For processes where direct measurement is impractical, sector benchmarks from industry associations or environmental permit databases provide a defensible estimation basis.

- Supplier questionnaires with tiered scope. Start with your top 20% of suppliers by spend or emission relevance. A focused questionnaire to this group often covers 70-80% of your Scope 3 category spend.

- Improvement roadmaps. Write a one-page plan stating which data gaps exist, what action you will take to close them (supplier portal, metering upgrades, procurement system integration), and by when. This plan becomes part of your sustainability statement.

Honest reporting with disclosed limitations is more credible than polished numbers with no methodology. Auditors know the difference, and so do sophisticated stakeholders.

A common pitfall is anchoring on proxy data without flagging it. A company that reports 12,400 tonnes of Scope 3 emissions with no disclosure of methodology gives the impression of precision it does not have. A company that reports the same number with a clear note that 60% is spend-based estimation using Exiobase factors, with a plan to reach 40% primary data by 2027, is far more credible and ESRS-compliant.

The sustainability reporting checklist covers the specific disclosure items you need to include when estimation is involved.

Pro Tip: Create an internal “data quality score” for each KPI. Rate each metric on a simple three-tier scale: primary measured data (tier 1), derived calculated data (tier 2), or proxy-based estimated data (tier 3). This makes it easy to prioritize improvement efforts and gives assurance providers a clear picture of where uncertainty lies.

Benchmarking, assurance, and KPI simplification

Once you’re gathering and estimating metrics, benchmarking and assurance add another layer of complexity.

Benchmarking CSRD KPIs against sector peers is valuable, but it requires care. Sector-aligned ESRS datapoints are essential for valid comparisons. A construction company benchmarking its GHG intensity against a chemicals manufacturer is comparing fundamentally different systems with different boundaries. Any cross-sector comparison must label its indicators clearly and state the calculation methodology used by each party.

Here is a framework for selecting benchmarkable KPIs:

| KPI category | Benchmarkable metric | Key condition for comparability |

|---|---|---|

| Climate | GHG intensity per revenue or unit produced | Same Scope boundary and emission factor vintage |

| Energy | Energy intensity per net revenue | Same organizational boundary |

| Water | Water intensity per unit output | Same withdrawal vs. consumption distinction |

| Waste | Circularity rate (recycled/total waste) | Same waste classification standard |

| Implementation | Reporting FTE, time to first disclosure | Comparable company size and scope |

For assurance readiness, here is what to prioritize:

- Traceability. Every KPI should trace to a source document or system record. Assurance providers will test a sample of your numbers back to origin.

- Internal review. Run an internal pre-assurance check where a person not involved in data collection verifies the calculations independently.

- Methodology documentation. Keep a living methodology note for each KPI, updated when calculation approaches change.

- Boundary consistency. Your ESRS KPI boundary must match your financial consolidation boundary unless you explicitly justify any deviation.

Assurance is not the finish line. It is the signal that your data management processes are mature enough to support external verification. Build toward it systematically, not reactively.

One important development to factor into your planning: ESRS simplification has reduced mandatory datapoints by 61%, while retaining the core climate, pollution, and circularity objectives. This is significant for mid-size companies in Romania that were concerned about reporting burden. It does not mean fewer KPIs necessarily, but it does mean your KPI design should focus on the retained mandatory items first, then layer in voluntary disclosures where they add strategic value.

For companies integrating Life Cycle Assessment (LCA) into their KPI strategy, the LCA for KPI strategies article explains how product-level environmental data can feed both ESRS reporting and commercial use cases like EPDs (Environmental Product Declarations).

Fresh perspective: Why true KPI usefulness depends on mapping, not measuring

Here is what we’ve observed across more than 158 projects in Romania and beyond: the companies that struggle most with CSRD KPIs are not the ones with the worst data. They are the ones that started measuring before they started mapping.

The instinct to act quickly is understandable. You pull together your energy invoices, run the carbon footprint calculation, and produce a number. That feels like progress. But if that number is not linked to a specific ESRS disclosure requirement, does not have a documented methodology, and has no improvement plan attached to it, it is compliance theater. It will not hold up to assurance, it will not support strategic decisions, and it will need to be rebuilt from scratch next year.

The disclosure-to-data mapping approach changes this entirely. You start with the ESRS requirement, work backward to identify the data you need, and design your collection process around that. This takes more time upfront. It creates better KPIs for life.

The business value of CSRD compliance goes beyond regulatory pass-marks. Companies that build genuine measurement infrastructure find it useful for energy procurement decisions, supplier negotiations, product pricing, and investor communications. The KPI is not just a compliance output. It is a decision-support tool, if you design it properly.

Our honest admission: mapping is harder and less satisfying in the short term than measuring. It requires cross-functional work between sustainability, finance, procurement, and operations teams. It surfaces uncomfortable gaps. It demands you write down what you do not yet know. But that discomfort is exactly what builds credibility over time. A sustainability statement full of well-documented uncertainties is far more trustworthy than one full of precise-looking numbers with no methodology behind them.

Rethink your KPI design as a regulatory mapping exercise first, and a measurement exercise second. That shift in sequence changes everything.

Solutions for CSRD-ready sustainability KPIs

Ready to design KPIs that deliver both compliance and operational impact? Here’s how ECONOS can help.

If the mapping-first approach resonates, the next step is practical implementation. At ECONOS, we help Romanian manufacturing and construction companies translate ESRS requirements into actionable KPI registers, with defined methodologies, documented estimation approaches, and year-one assurance readiness built in.

Our work covers the full range: carbon footprint assessment across all three Scopes, ESG reporting solutions aligned to CSRD and ESRS requirements, EU taxonomy guidelines for capital allocation reporting, and full sustainability consulting Romania for companies building internal capacity. Through ECONOS Academy and our AI-powered assistant AVA, we build your team’s ability to run these processes independently, not just deliver a report and leave. If you’re facing a first disclosure deadline or rebuilding a KPI framework that did not hold up, we’re ready to work through it with you.

Frequently asked questions

What is the first step to implementing sustainability KPIs for CSRD?

Start by mapping KPIs to ESRS disclosure requirements, defining calculation boundaries and methodologies before you begin data collection. This mapping step determines which data you actually need and prevents costly rework later.

How do you handle missing value-chain data when reporting KPIs?

Use proxy metrics or sector averages, and disclose your estimation approaches including data sources, accuracy level, and a documented plan to improve coverage over time. ESRS expects transparent reporting of limitations, not perfect data from day one.

Which environmental KPIs are most critical for manufacturing under ESRS?

Climate (energy and Scope 1–3 emissions), pollution, water use, and circularity/resource use are the primary ESRS KPI groupings for manufacturing, with Scope 3 typically representing the largest data challenge.

What changes in ESRS KPI structure should you be aware of for 2026?

ESRS simplification has reduced mandatory datapoints by 61%, focusing disclosure requirements on core climate, pollution, and circularity objectives while reducing overall reporting burden for mid-size companies.

Can you compare CSRD KPIs across sectors in Romania?

Yes, but comparisons must use sector-aligned ESRS datapoints or clearly distinguish implementation indicators from compliance metrics to avoid non-equivalent benchmarks that mislead stakeholders.