.png)

TL;DR:

- Scope 3 emissions account for 70-95% of most companies’ total greenhouse gases.

- Understanding and managing Scope 3 is essential for ESG compliance and supply chain transparency.

- Measuring Scope 3 involves tiered methods, stakeholder engagement, and addressing data quality challenges.

For most mid-sized and large companies, Scope 3 represents 70-95% of their total greenhouse gas footprint. That number tends to surprise people. Leaders who have invested in clean energy and efficient operations often discover that the emissions they don’t directly control dwarf everything else combined. Scope 3 covers your supply chain, your customers’ product use, employee travel, and much more. If you’re serious about ESG compliance, carbon footprint reduction, or meeting investor expectations, understanding and managing Scope 3 isn’t optional. This article breaks down what Scope 3 means, why it dominates GHG accounting, and how to approach it strategically.

Table of Contents

- What are Scope 3 emissions and why do they matter?

- How Scope 3 shapes ESG reporting and compliance

- Practical methodologies for calculating Scope 3 emissions

- Challenges, nuances, and best-practice strategies

- A practical view: Why Scope 3 isn’t just a reporting obligation

- Get expert help for your Scope 3 and ESG journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Scope 3 is dominant | Up to 95% of your company’s emissions come from Scope 3 sources that are often overlooked. |

| ESG compliance requires Scope 3 action | European laws and investor pressures mean Scope 3 data must be audit-ready and transparent. |

| Prioritize material categories | Start with your largest emission sources for high-impact and efficient ESG improvements. |

| Choose the right methodology | Using supplier-specific or hybrid methods yields more accurate results and better compliance. |

| Supplier engagement is key | Reliable Scope 3 accounting and reduction depend on collaboration with your value chain partners. |

What are Scope 3 emissions and why do they matter?

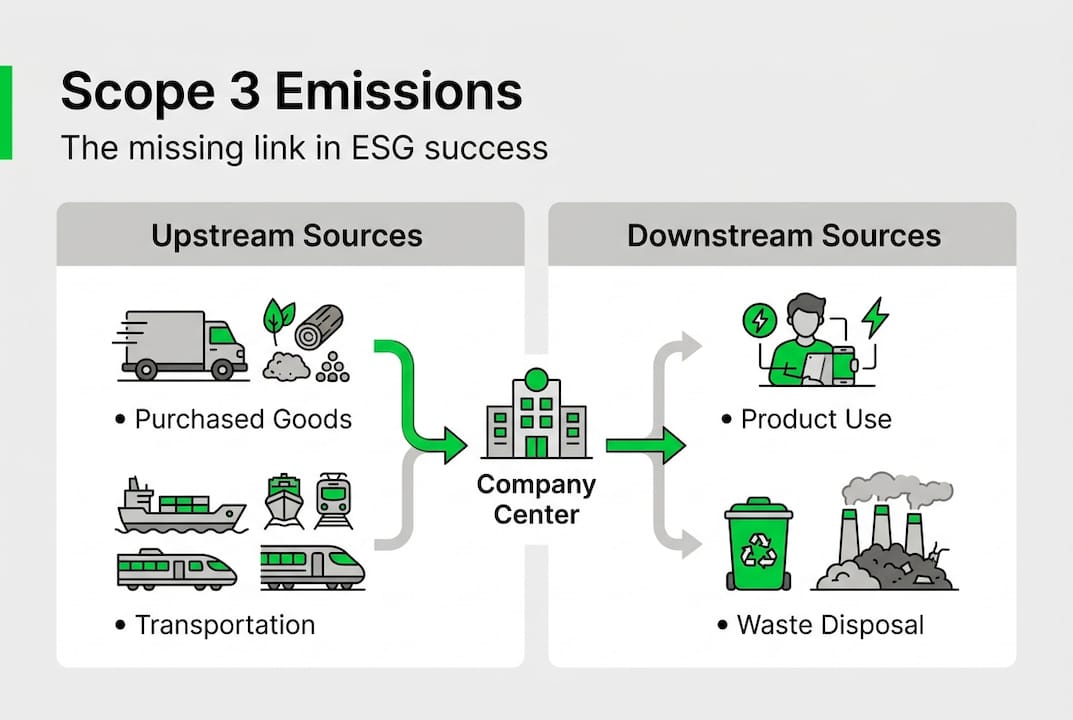

The Greenhouse Gas Protocol divides corporate emissions into three scopes. Scope 1 covers direct emissions from owned sources. Scope 2 covers purchased energy. Scope 3 covers everything else, meaning all indirect emissions that occur upstream or downstream in your value chain but are not under your direct operational control.

Scope 3 is divided into 15 categories. Upstream categories include:

- Purchased goods and services (often the single largest category)

- Capital goods

- Fuel and energy-related activities

- Upstream transportation and distribution

- Waste generated in operations

- Business travel

- Employee commuting

- Upstream leased assets

Downstream categories include use of sold products, end-of-life treatment, downstream transportation, franchises, and investments.

Understanding carbon footprint basics helps clarify why these categories matter so much. For consumer goods companies, the use of sold products alone can account for more than 60% of total emissions. For retailers, purchased goods dominate. For chemical manufacturers, upstream raw material extraction is the critical driver.

The data is consistent: Scope 3 exceeds 80% of total company emissions across most industries, according to CDP benchmarks. Romanian distribution company AQUILA expanded its Scope 3 reporting in 2024, recognizing that upstream logistics and purchased goods were where the real numbers lived.

| Industry | Typical Scope 3 share |

|---|---|

| Consumer goods | 85-95% |

| Retail | 80-90% |

| Chemicals | 70-85% |

| Financial services | 90-95% |

Ignoring Scope 3 means reporting on a fraction of your actual impact. Companies that follow ESG best practices know that credibility in sustainability requires full value-chain transparency, not just what happens inside the fence.

How Scope 3 shapes ESG reporting and compliance

With a foundational understanding of Scope 3, it’s vital to see how it factors into the expanding ESG regulatory landscape.

The CSRD requirements are reshaping what European companies must disclose. Under the Corporate Sustainability Reporting Directive, large companies must apply a double materiality assessment, which evaluates both how climate issues affect the business and how the business affects the climate. In most cases, Scope 3 passes both tests. That means it’s material and must be reported.

Key compliance milestones for companies in Romania and the EU:

- Large public-interest entities with over 500 employees: reporting from fiscal year 2024 onward

- Large companies not previously covered: reporting from fiscal year 2025

- Listed SMEs: phased relief until 2026, with simplified standards

- All covered companies: audit-ready, third-party verified data required

The practical difficulty is real. Scope 3 data requires granular supplier information, consistent emission factors, and systems that can handle large volumes of inputs. Many companies discover their software isn’t ready. Others find their procurement teams have never been asked to collect this kind of data before.

“Double materiality often deems Scope 3 material for large companies. Phased relief exists for SMEs, but large firms need audit-ready data by 2026 under CSRD.”

Scope 3 also directly affects ESG ratings from agencies like CDP, MSCI, and EcoVadis. Investors increasingly screen for climate credibility, and a company that reports only Scope 1 and 2 raises red flags. If you want to understand the full scope of ESG reporting challenges your organization may face, it helps to start with Scope 3 data readiness.

SBTi (Science Based Targets initiative) adds another layer. If Scope 3 represents more than 40% of your total emissions, SBTi requires you to set a Scope 3 target. For most companies, that threshold is crossed easily.

Pro Tip: Don’t wait for a regulator to ask. Run a preliminary Scope 3 screening now, even with rough spend-based estimates. It tells you where to focus and gives you a head start on EU regulations compliance.

Practical methodologies for calculating Scope 3 emissions

Navigating regulatory requirements only gets you so far. Let’s break down how to actually measure Scope 3 emissions with confidence.

The GHG Protocol defines four calculation methods, each suited to different situations:

| Method | Accuracy | Best use case | Data intensity |

|---|---|---|---|

| Supplier-specific | Highest | Material categories with engaged suppliers | High |

| Hybrid | High | Mix of primary and secondary data | Medium-high |

| Average-data | Medium | Categories with reliable sector averages | Medium |

| Spend-based | Lowest | Initial screening, data-scarce categories | Low |

Here’s a practical starting sequence when resources are limited:

- Run a spend-based screening across all 15 categories to identify your top emitters by rough magnitude.

- Prioritize the top 3-5 categories that represent the bulk of estimated emissions.

- Engage key suppliers in those categories to request primary activity data or product carbon footprints (PCFs).

- Apply average-data or hybrid methods for secondary categories where supplier data isn’t yet available.

- Iterate annually, improving data quality in material categories over time.

Supplier engagement is where the real accuracy gains happen. Frameworks like PACT for PCF exchange allow companies to share verified product-level carbon data across supply chains, reducing reliance on generic emission factors.

For companies exploring Scope 4 consulting, understanding Scope 3 methodology first is essential, since avoided emissions calculations build directly on the same data infrastructure.

Pro Tip: Use digital tools that support PCF data exchange. Platforms built on open standards let your suppliers push verified emission data directly into your accounting system, cutting manual effort and improving accuracy significantly.

Challenges, nuances, and best-practice strategies

Now that methods are clear, the last area to address is the real-world obstacles and the best ways to manage them.

The most common challenge is supplier data quality. Most small and mid-sized suppliers have never calculated their own carbon footprint, let alone a product-level one. You’ll often receive estimates, outdated figures, or nothing at all. This is normal. The answer isn’t to wait for perfect data. It’s to be transparent about uncertainty and improve iteratively.

Other common obstacles include:

- Category screening complexity: Deciding which of the 15 categories are material requires judgment and defensible methodology.

- Biogenic and land-use emissions: Guidance is improving but still inconsistent across frameworks, making agriculture and forestry-related categories particularly tricky.

- Investments (Category 15): Often excluded if immaterial, but financial institutions and holding companies need to address this directly.

- Hard-to-abate areas: Some upstream processes have no clean alternatives yet, requiring honest disclosure rather than premature claims.

According to Scope 3 reporting guidance, not all 15 categories are required. Materiality screening allows you to exclude categories that are genuinely not significant to your business, provided you document and disclose the rationale clearly.

“Transparency about what you don’t know is not a weakness. It’s the foundation of credible reporting.”

Leading companies build supplier engagement programs rather than one-off data requests. They provide templates, training, and sometimes direct support to help key suppliers measure their own footprints. This builds loyalty, improves data quality, and accelerates reducing Scope 3 emissions across the value chain.

Pro Tip: Start with your largest emission categories and iterate. A credible 70% coverage with honest uncertainty disclosures is far more valuable than a polished report that quietly omits half the picture.

A practical view: Why Scope 3 isn’t just a reporting obligation

With this practical foundation, let’s step back for a candid view on how Scope 3 fits into the bigger picture.

We’ve worked with enough companies to say this plainly: the organizations that treat Scope 3 as a compliance checkbox miss the point entirely. Yes, SBTi requires Scope 3 targets when it exceeds 40% of total emissions. Yes, CSRD auditors will ask for it. But the real value isn’t in the report.

Scope 3 forces you to understand your supply chain in ways that most procurement teams never have. That understanding surfaces cost inefficiencies, supplier risks, and market opportunities that have nothing to do with carbon. Companies that engage suppliers on emissions data often discover quality issues, logistics redundancies, and sourcing alternatives simultaneously.

Carbon credits are sometimes presented as a solution for hard-to-abate Scope 3 categories. We’d caution against leaning on them too heavily. They’re a partial tool, not a strategy. The debate on carbon credits in Scope 3 accounting is ongoing, and credible frameworks are tightening the rules on what counts.

What leading companies do differently is prioritize engagement, data quality, and continuous improvement over perfection in year one. They publish honest reporting strategies, acknowledge gaps, and show a trajectory. That approach builds more trust with investors and customers than a polished but incomplete disclosure ever could.

Get expert help for your Scope 3 and ESG journey

Scope 3 accounting is genuinely complex, and getting it right requires the right methodology, the right data strategy, and a clear understanding of what regulators and raters actually expect.

At ECONOS, we’ve guided companies like Michelin, eMAG, and Raiffeisen Bank through exactly this process. Our approach to carbon footprint assessment builds your internal capacity rather than creating dependency on consultants. We help you identify material categories, engage suppliers, and produce audit-ready data. When you’re ready to move from measurement to action, our ESG reporting services keep you compliant, credible, and ahead of the curve.

Frequently asked questions

Which Scope 3 categories are most important for European companies?

Purchased goods and services, upstream transportation, and use of sold products are typically the largest categories for European companies, though exact rankings vary by industry.

Can we exclude categories from Scope 3 reporting if data is unavailable?

You may exclude a category if it is not material to your business, but GHG Protocol guidance requires you to document and disclose the rationale for any exclusion.

How does Scope 3 influence ESG ratings and investor interest?

Scope 3 transparency improves ESG ratings from agencies like CDP and EcoVadis, and signals to investors that your climate strategy is credible and forward-looking.

What if our suppliers can’t provide Scope 3 data?

You can use sector averages or spend-based methods as interim steps, while gradually building supplier engagement programs to improve data quality over time.