.png)

TL;DR:

- ESRS is a complex layered system with over 1,000 data points impacting roughly 50,000 EU companies.

- Companies must assess double materiality, covering both financial risks and environmental/social impacts, annually.

- Simplifications and interoperability efforts reduce data burdens but require careful judgment and sector benchmarking.

ESRS is not a single reporting standard. It is a layered system of obligations that spans over 1,000 data points and touches roughly 50,000 companies across the EU. For mid-size and large companies in Romania and France, the pressure is real and immediate. Thresholds are shifting, value chain obligations are expanding, and the double materiality assessment adds a layer of complexity that most internal teams have never dealt with before. This guide cuts through the noise and gives you a practical, honest map of what ESRS requires, who it applies to, and how to approach compliance without losing your footing.

Table of Contents

- Who must comply and current thresholds

- Core ESRS structure — cross-cutting and topical standards

- Double materiality and methodologies — DMA and value chain

- Environmental and social disclosures — practical guidance

- What most articles miss: How simplifications and interoperability impact real compliance

- How ECONOS helps with ESRS compliance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand ESRS scope | Check your company size and status to determine whether ESRS applies and watch for rising thresholds in France and Romania. |

| Organize disclosures | Map out mandatory cross-cutting and topical ESRS requirements to streamline your management reporting. |

| Master double materiality | Use the DMA process to identify which impacts and financial risks need reporting, reviewing annually for changes. |

| Leverage relief options | Apply phased-in disclosures and relief measures for SMEs and value chain participants, especially Scope 3 exemptions. |

| Prepare for digital and assurance | Digitally tag all ESRS data and anticipate assurance requirements, transitioning from limited to reasonable over four years. |

Who must comply and current thresholds

Not every company is in scope at the same time, but more are entering the picture than many realize. Under CSRD, ESRS applies to large companies that meet at least two of three criteria: more than 250 employees, more than €50 million in turnover, or more than €25 million on the balance sheet. These are the current thresholds, but proposed Omnibus amendments would raise the bar significantly, to more than 1,000 employees and more than €450 million in turnover.

In France, the directive was transposed through Ordinance 2023-1142, which introduced a phased schedule for different company categories. Large listed companies reported first, followed by large non-listed companies, and some SMEs benefit from initial exemptions. In Romania, transposition has followed a similar EU-mandated timeline, with national regulators adapting requirements to local corporate law.

Here is a summary of key applicability rules for both countries:

- Large listed companies (EU-regulated markets): reporting started for fiscal year 2024

- Large non-listed companies: reporting starts for fiscal year 2025

- Listed SMEs: reporting starts for fiscal year 2026, with opt-out until 2028

- Third-country subsidiaries: in scope if EU net turnover exceeds €150 million

- Value chain companies: may face indirect obligations through customer or supplier requests

| Criteria | Current threshold | Proposed 2026 threshold |

|---|---|---|

| Employees | >250 | >1,000 |

| Annual turnover | >€50M | >€450M |

| Balance sheet | >€25M | >€25M (unchanged) |

| Must meet | At least 2 of 3 | At least 2 of 3 |

Even if your company falls below the updated thresholds, you may still face indirect pressure. Large customers already in scope will request sustainability data from their suppliers, regardless of whether those suppliers are formally required to report. Understanding the business value of CSRD compliance early helps you respond to those requests strategically rather than reactively.

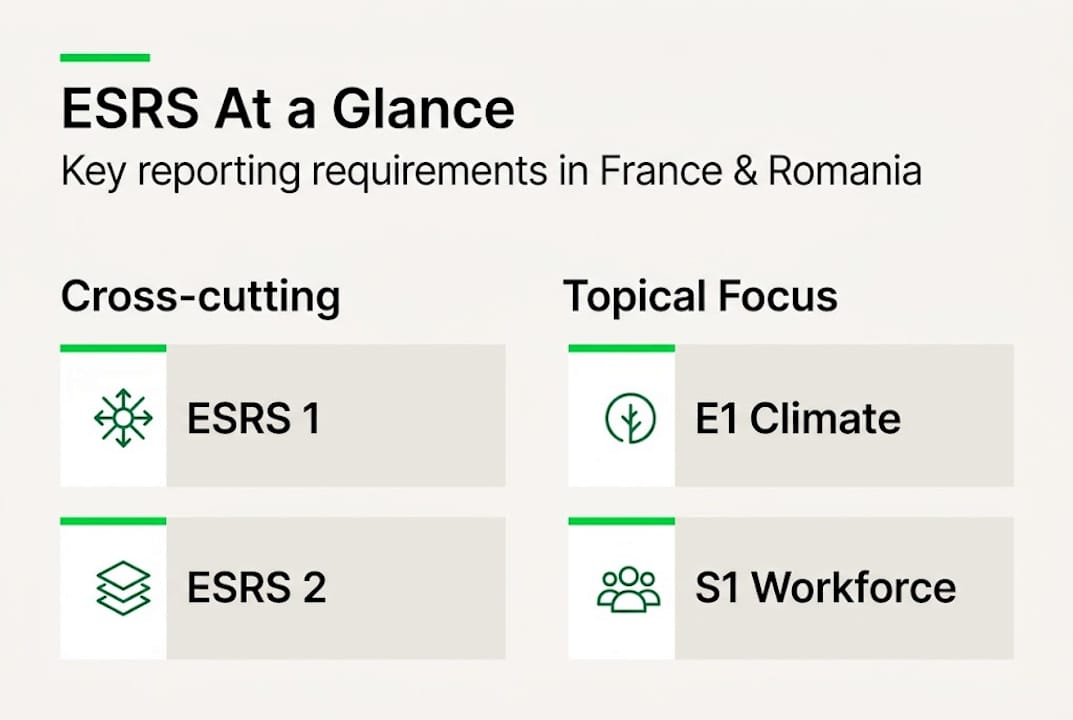

Core ESRS structure — cross-cutting and topical standards

Once you know you are in scope, the next question is: what exactly do you need to report? ESRS is structured around mandatory cross-cutting standards and a set of topical standards covering environment, social, and governance topics.

ESRS 1 sets the general principles and architecture of the framework. ESRS 2 is the mandatory disclosure standard that every company must apply, covering governance, strategy, impact and risk management, and metrics and targets. Think of ESRS 2 as the spine of your report.

The topical standards are:

- E1 to E5: Climate change, pollution, water and marine resources, biodiversity, and resource use

- S1 to S4: Own workforce, workers in the value chain, affected communities, and consumers

- G1: Business conduct

Not all topical standards apply automatically. Your double materiality assessment (explained in the next section) determines which ones are relevant to your business. Reporting must cover governance, strategy, impacts, risks, opportunities, metrics, and targets for each material topic.

Here is a practical sequence for structuring your ESRS report:

- Complete your double materiality assessment to identify which topics are material

- Map material topics to the relevant ESRS topical standards

- Collect quantitative and qualitative data for each required disclosure

- Draft the sustainability statement as part of the management report

- Apply XBRL digital tagging to all disclosures for regulatory submission

- Arrange for limited assurance from an accredited auditor

| Standard type | Examples | Mandatory? |

|---|---|---|

| Cross-cutting | ESRS 1, ESRS 2 | Yes, for all in-scope companies |

| Topical (environment) | E1 climate, E2 pollution | If material per DMA |

| Topical (social) | S1 workforce, S4 consumers | If material per DMA |

| Topical (governance) | G1 business conduct | If material per DMA |

Pro Tip: Start harmonizing your internal reporting systems now. XBRL digital tagging requires structured, consistent data. If your sustainability data lives in spreadsheets across five departments, the tagging process will be painful. Align your ESG reporting requirements and data collection workflows before the deadline arrives.

Double materiality and methodologies — DMA and value chain

Double materiality is the concept that separates ESRS from most other frameworks. It requires companies to assess sustainability topics from two directions: how sustainability issues create financial risks or opportunities for the company (financial materiality), and how the company’s activities impact people and the environment (impact materiality). Both lenses must be applied.

DMA is the first step in the ESRS process, and it requires an annual review. The assessment uses qualitative and quantitative thresholds to evaluate the severity and likelihood of impacts, as well as the magnitude of financial effects. This is not a one-time exercise.

Here is a practical sequence for running your DMA:

- Identify your full list of sustainability topics across the ESRS framework

- Assess each topic for impact materiality (severity, scale, scope, reversibility) and financial materiality (likelihood and magnitude of financial effect)

- Document your rationale clearly, including what you excluded and why

- Integrate material topics into your reporting structure and governance processes

- Review annually, updating for new business activities, regulatory changes, or stakeholder feedback

Value chain coverage is another area where companies often underestimate the scope. Coverage is phased over four years, with relief provisions for SMEs and cases where materiality overrides apply. In the first reporting year, companies are not required to collect full Scope 3 value chain data if it is not yet available, but they must explain the gap.

Field test findings from EFRAG showed that companies found DMA the most resource-intensive part of ESRS implementation. Simplifications in the 2025 amendments help, but the core logic of double materiality remains unchanged. Companies that treated DMA as a checkbox exercise early on are now revisiting their work.

Pro Tip: Document your materiality rationale in detail, not just the conclusions. Auditors will ask why certain topics were excluded. A clear, traceable methodology protects you during assurance and makes annual updates far easier. Reviewing ESG supply chain examples from peers in your sector can help you calibrate your own value chain scope.

Environmental and social disclosures — practical guidance

Once your DMA is complete, you know which topical standards apply. Here is what the most commonly material topics actually require.

On the environmental side, E1 (climate change) is almost universally material. It requires climate transition plans, Scope 1 to 3 greenhouse gas emissions, and energy mix reporting for companies where these are material. E2 covers pollution to air, water, and soil. E3 addresses water and marine resources. E4 covers biodiversity and ecosystems, which is increasingly scrutinized. E5 addresses resource use and the circular economy.

On the social side, S1 (own workforce) requires disclosures on working conditions, equal treatment, and living wages. S2 covers workers in the value chain. S3 addresses affected communities. S4 covers consumers and end-users.

Required metrics across these topics include:

- GHG emissions: Scope 1, 2, and 3 in tonnes of CO2 equivalent

- Energy consumption: total and renewable share

- Water withdrawal and consumption: by source and stress area

- Waste generated: by type and disposal method

- Workforce composition: by gender, contract type, and region

- Living wage gap: percentage of employees below living wage benchmarks

- Health and safety: injury rates and lost-time incidents

For mid-size companies and those in the value chain, relief options exist for VSMEs and first-year reporters. Scope 3 data collection can be phased in, and there are caps on how much data large companies can request from SME suppliers. This does not mean you can skip Scope 3 entirely. It means you have time to build the capability. Starting now with Scope 3 emissions guidance is far better than scrambling later.

What most articles miss: How simplifications and interoperability impact real compliance

Most ESRS guides focus on what the standards require. Fewer talk honestly about what the simplification trend actually means for companies trying to comply in good faith.

The 2025 Omnibus amendments and EFRAG’s draft revisions reduce the datapoint burden significantly, which sounds like good news. And it is, to a point. But companies that design their reporting around the minimum required disclosures risk missing the granularity that investors, banks, and large customers actually want. Simplification does not mean less scrutiny. It means more discretion, and discretion requires judgment.

Interoperability with GRI, ISSB, and EU Taxonomy is praised in policy documents. In practice, mapping between frameworks takes real effort. Concepts that appear equivalent often carry different definitions, boundaries, or calculation methods. We have seen companies in both Romania and France assume that a GRI-aligned report would satisfy ESRS requirements with minor adjustments. That assumption is usually wrong.

Our advice: use early reporters in your sector as practical reference points, not just the official ESG news and updates. Read their sustainability statements. See what they disclose, how they frame DMA, and where they acknowledge gaps. That is more useful than any rulebook summary.

How ECONOS helps with ESRS compliance

ESRS compliance is a serious undertaking, and the companies that handle it well are the ones that build internal capability rather than outsourcing every decision.

At ECONOS, we help mid-size and large companies in Romania and France move from confusion to clarity on comprehensive ESG reporting. We support double materiality assessments, Scope 1 to 3 footprint assessment, and EU taxonomy solutions that connect your environmental data to your financial disclosures. What makes our approach different is that we train your team to own the process. You understand what you are reporting and why, which means you are ready for auditors, investors, and the next regulatory update.

Frequently asked questions

Which companies in France and Romania must comply with ESRS under CSRD?

Companies meeting at least two of three thresholds — employee count, turnover, or balance sheet — are required to comply, with rising thresholds from 2026 amendments raising the employee bar to more than 1,000 and turnover to more than €450 million.

What is meant by ‘double materiality’ in ESRS reporting?

Double materiality assesses both how sustainability issues affect the company financially and how the company impacts the environment and society, with annual qualitative and quantitative review required under ESRS 1.

Are SMEs in the value chain required to provide full ESRS disclosures?

SMEs and VSMEs face partial or voluntary disclosures, with a cap on data requests from large companies and phased-in relief for Scope 3 data in the first reporting year.

How do companies report ESRS data and what assurance is required?

ESRS data must be digitally tagged using XBRL within the management report and undergo limited assurance, with a planned transition to reasonable assurance after four years.

Where can companies find benchmarks or sector guidance for ESRS disclosures?

Peer sector reports from early reporters and GRI/ISSB interoperability mappings are the most practical starting points, though country-specific guidance for Romania and France remains limited.