.png)

TL;DR:

- Most sustainability audits fail not due to bad intentions but because evidence is scattered, ownership is unclear, and preparation is late. To achieve audit readiness, companies must establish systems, documentation, and team coordination well before external review, focusing on scope definition, evidence management, and internal verification. Embedding these practices into ongoing operations ensures smoother audits, better compliance, and continuous improvement.

Most sustainability audits don’t fail because companies have bad intentions. They fail because evidence is scattered across departments, data ownership is unclear, and preparation starts too late. Learning how to prepare a sustainability audit means building the systems, documentation, and team coordination long before an auditor walks in the door. This guide gives Quality, HSE, and Sustainability Managers a structured path through scope definition, evidence management, internal verification, and reporting. Every section addresses the real-world obstacles that derail even well-funded programs.

Table of Contents

- Key takeaways

- How to prepare a sustainability audit: scope and requirements

- Building your audit evidence pack

- Conducting an internal pre-audit review

- Preparing the final audit report

- Common pitfalls and how to avoid them

- My take on what actually separates audit-ready organizations

- Ready to make your next audit your cleanest one yet?

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Define scope before collecting data | Identify sites, emission scopes, and material topics first to avoid wasting effort on irrelevant evidence. |

| Build a centralized evidence pack | Map every KPI to source documents, emission factors, and approvals to create a defensible audit trail. |

| Run an internal pre-audit | Simulate auditor procedures internally to find and resolve gaps before external review begins. |

| Assign explicit data ownership | Each data stream needs a named owner with a deadline to prevent last-minute scrambles. |

| Structure findings clearly | Final audit reports should include KPI tables, methodology notes, and prioritized recommendations. |

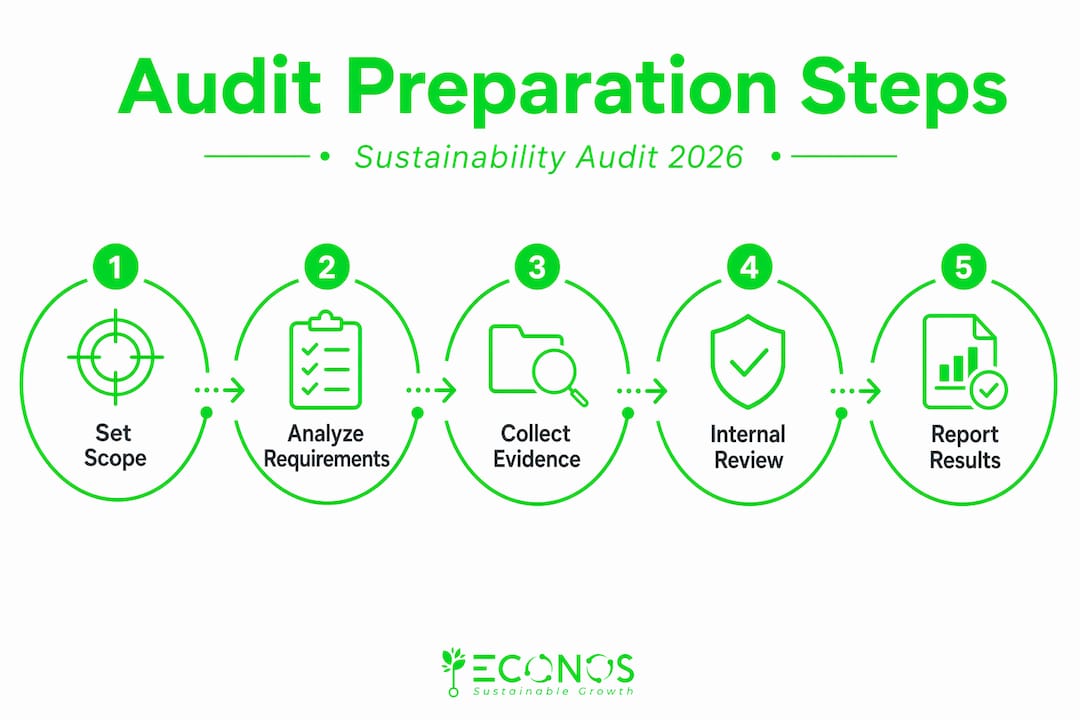

How to prepare a sustainability audit: scope and requirements

The first and most overlooked step is not data collection. It is deciding what the audit actually covers. Without a defined scope, teams collect the wrong data, argue over boundaries during fieldwork, and hand auditors a fragmented picture.

Start by analyzing your regulatory, industry, and corporate requirements. If you operate under the EU’s Corporate Sustainability Reporting Directive, the ESRS standards dictate which topics are material. If you are preparing for an EcoVadis assessment or third-party assurance under ISSA 5000, the criteria differ. Know which framework governs your audit before anything else.

Next, document your scope boundaries for emissions clearly. Define which sites fall under the audit, whether Scope 3 categories are included, and which parts of the supply chain are in or out. Write down the inclusion and exclusion criteria and keep them on file. Auditors will ask.

Once scope is defined, identify material topics and the KPIs attached to them. For a manufacturing company, that might mean energy intensity, water withdrawal, and lost-time injury rate. For a logistics firm, fleet emissions and carrier data dominate. Tailor your sustainability audit checklist to the specific risk profile of your sector, not a generic template.

Assign audit roles before data collection starts. This means naming who leads the audit, who owns each data stream, and who approves final evidence packages. Clarity here is not bureaucracy. It is the difference between a smooth process and a last-minute panic.

- Confirm which regulatory or certification framework applies to your audit

- Define Scope 1, 2, and Scope 3 boundaries with documented rationale

- Identify material topics relevant to your sector and stakeholder expectations

- List KPIs for each material topic with target values and baseline data

- Assign named owners for each data stream with submission deadlines

Pro Tip: Schedule a one-hour kick-off meeting with all data owners before any collection begins. Walk through the scope document together. Misalignments caught in week one cost far less than those discovered during external fieldwork.

Building your audit evidence pack

Once scope is set, the real work begins. An audit evidence pack is a structured collection of every document, data file, calculation, and policy an auditor will need to form an opinion. Think of it as a parallel file system designed around audit logic rather than your internal folder structure.

Start with policies and procedures. Collect your environmental policy, HSE management system documentation, sustainability targets, and any commitments made in public reports. These establish context. Auditors want to see that performance data sits inside a governed framework, not floating in spreadsheets.

Then move to source documents. Utility bills, fuel purchase invoices, refrigerant top-up records, waste disposal contracts, and training attendance logs all qualify as primary evidence. Do not substitute a summary slide for a source document. Auditors seek a data trail and repeatable methods across all relevant scopes. A polished presentation without the underlying source files will generate a qualified opinion or outright failure.

Build a documentation index. This is the backbone of your evidence pack.

| KPI | Source document | Calculation method | Emission factor | Approved by |

|---|---|---|---|---|

| Scope 1 natural gas | Monthly invoices (Jan–Dec) | Volume × IPCC factor | 2.204 kg CO₂e/m³ | HSE Director |

| Scope 2 electricity | Grid bills + renewable certificates | Location-based | IEA country average | Energy Manager |

| Scope 3 business travel | Expense reports + flight logs | Distance × EF by class | DEFRA 2025 | Finance Lead |

| Water withdrawal | Meter readings + municipal invoices | Direct measurement | N/A | Facility Manager |

This table format forces alignment between what you report and what you can prove. Explicit ownership for each data stream prevents the common scenario where no one can locate the original file during audit week.

Standardize your data collection templates across sites. When the same format captures electricity consumption in Bucharest and in Hanoi, aggregation becomes clean and calculation errors drop. Use version control on all templates. Date-stamp every revision and log who changed what and why.

Pro Tip: Create a “confidence rating” column in your documentation index. Mark each KPI as high, medium, or low confidence based on evidence quality. Low-confidence items become your pre-audit priority list.

- Compile policies, targets, and management system documentation first

- Collect source documents: invoices, meter readings, contracts, training logs

- Build a documentation index linking each KPI to source, method, factor, and approver

- Standardize templates across all sites and reporting periods

- Implement version control and change logs for all data files

Conducting an internal pre-audit review

Before any external auditor arrives, run your own. An internal pre-audit simulates actual auditor procedures and exposes weaknesses you have the time and authority to fix. This is one of the most underused sustainability audit best practices, and one of the highest-return activities in the entire preparation process.

Here is a practical sequence for running an internal pre-audit:

- Appoint an internal lead who was not directly responsible for data collection. Independence matters. Someone too close to the data will rationalize gaps rather than flag them.

- Verify data completeness by checking that every KPI in your documentation index has a source file attached. Missing evidence for even one material indicator can compromise the entire audit opinion.

- Test data traceability by picking five KPIs at random and tracing them from the reported number back to the original source document. If you cannot complete that trace in under ten minutes, the auditor will not be able to either.

- Check for internal consistency across documents. Does the total energy reported in your ESG report match the sum of site-level utility invoices? Discrepancies at this stage are opportunities. Discovered during external audit, they become findings.

- Document methodologies, assumptions, and scope boundaries in a written methodology note. Include any changes made since the previous reporting period and the rationale behind them. Formal controls for data revisions are what keep comparability intact across years.

- Brief all involved staff on their role in the audit process. Data owners should know which files to provide, in what format, and within what timeframe. Teams that understand audit requirements respond faster and with fewer errors.

Transparent communication at this stage matters more than most managers expect. When the finance team understands why you need original invoices rather than a summary report, they prioritize accordingly. When the facilities team knows what an auditor will ask about refrigerant leakage, they keep records proactively.

For companies preparing for EU sustainability audits under ISSA 5000 assurance, the internal review must also demonstrate that controls, competence, and sufficient evidence exist before engagement begins. The standard is explicit: auditor readiness is a precondition, not an afterthought.

Pro Tip: Document every gap you find during the internal pre-audit, even ones you fix immediately. That gap register becomes evidence of your internal control process and demonstrates governance to the external auditor.

Preparing the final audit report

The audit process does not end when evidence collection closes. How you compile and communicate findings shapes how the audit is perceived by leadership, regulators, and external stakeholders. Clear reports with KPIs, scope definitions, and prioritized recommendations are what turn a compliance exercise into a continuous improvement tool.

Structure your report around the following elements:

- Executive summary with key findings, material topics covered, and overall performance against targets

- Scope and methodology section explaining boundaries, emission factor sources, calculation approaches, and any restatements from prior periods

- KPI performance table showing actuals against baseline and target, with trend direction

- Findings section divided into strengths, gaps, and risk implications. Be honest here. An audit report that glosses over weaknesses loses credibility with sophisticated readers and does nothing to improve performance.

- Recommendations prioritized by impact and feasibility. A high-impact, low-cost fix gets addressed before a high-impact, high-cost one. Give each recommendation an owner and a timeline.

- Approval log documenting who reviewed the report and when. Formal sign-off processes with documented checklists assure auditors that data underwent thorough internal validation before publication.

Coordinate with your communications team before the report goes public. Sustainability disclosures are increasingly scrutinized for greenwashing. Every claim in the external version of your report needs to be traceable to the audit evidence pack. If a claim cannot be supported by source evidence, it should not appear.

Common pitfalls and how to avoid them

Common audit failures cluster around a predictable set of problems: fuzzy scope boundaries, unsupported estimates, scattered evidence, and informal controls. Knowing the pattern lets you intercept it before it costs you.

| Common pitfall | What it looks like | How to address it |

|---|---|---|

| Unclear Scope 3 boundaries | Different teams report different category inclusions | Document inclusion/exclusion criteria in writing before data collection |

| Unsupported estimates | Figures in reports lack original source files | Replace estimates with measured data or document estimation methodology in full |

| Scattered evidence | Files spread across email, shared drives, and personal laptops | Centralize all evidence in a single platform with access controls |

| Informal change controls | Data corrections made without documentation | Implement a change log requiring rationale and approver sign-off for every revision |

| Multi-department conflicts | Finance and operations report different energy figures | Establish a single source of truth for each data stream with a named owner |

Technology helps, but only if it is implemented with discipline. A centralized platform for supply chain data and real-time emission tracking reduces manual errors and makes traceability automatic rather than manual.

Pro Tip: Before your next audit cycle, ask your team: “If an auditor asked for the original source file for our Scope 1 total right now, how long would it take to find it?” The honest answer tells you exactly where your evidence management needs work.

My take on what actually separates audit-ready organizations

I have worked with organizations across manufacturing, banking, and retail. The ones that consistently pass audits without last-minute stress share one trait: they treat audit preparation as an ongoing business process, not an annual event.

What I’ve found is that the data is rarely the real problem. Most companies generate enough raw data to support a credible audit. The failure points are ownership and structure. When no one is specifically accountable for, say, refrigerant records, those records disappear into someone’s inbox and resurface only under pressure.

I’ve seen companies with genuinely strong environmental performance receive qualified audit opinions because their documentation was disorganized. I’ve also seen companies with modest performance pass cleanly because their evidence pack was airtight and their methodology note was thorough. Auditors follow the paper trail. Build a good one.

Technology has changed this work meaningfully. Platforms that centralize emission data and automate traceability have cut preparation time significantly for our clients. But I’d caution against thinking a software subscription solves a governance problem. The tool works when ownership and process are already in place.

What differentiates the best organizations is that their ESG workflow is embedded in how they operate, not bolted on at reporting time. That shift takes a year or two to build. Start now.

— Mathieu

Ready to make your next audit your cleanest one yet?

Audit preparation is genuinely difficult when you are managing it alongside day-to-day operations. At Econos-esg, we help Quality, HSE, and Sustainability Managers build the systems that make audits repeatable and defensible, not stressful.

Our work covers carbon footprint assessment with full Scope 1, 2, and 3 documentation, ESG reporting services aligned with CSRD and ESRS, and EcoVadis certification support for companies preparing for supplier evaluations. We also help companies align with EU Taxonomy requirements before auditors raise the question. If you want to understand where your audit readiness stands today, our team is a straightforward conversation away.

FAQ

What does a sustainability audit checklist include?

A sustainability audit checklist covers policies, KPIs, source documents, emission factor references, calculation methodologies, scope boundaries, and approval records. Each item should be traceable from the reported figure back to its original source file.

How do you define scope for a sustainability audit?

Define scope by documenting which sites, operations, and emission categories (Scope 1, 2, and 3) are included and excluded, along with the written rationale for each boundary decision. This documentation prevents disputes during external audit fieldwork.

How long does it take to prepare for an environmental audit?

For most mid-size companies, thorough audit preparation takes three to six months when starting from scratch. Organizations with centralized data systems and named data owners can reduce that significantly by focusing only on gap closure.

What makes a sustainability audit fail?

Scattered evidence, unsupported estimates, and unclear scope boundaries are the most common causes of audit failure or qualified opinions. Poor governance, not poor performance, is usually the root cause.

How do EU sustainability audit requirements differ from standard audits?

EU sustainability audits conducted under CSRD and ESRS require third-party assurance and must demonstrate that internal controls, competence, and documentary evidence meet the ISSA 5000 standard before the engagement begins. The bar for evidence quality is higher than most voluntary frameworks.