.png)

TL;DR:

- Aligning with EU sustainability standards involves mastering ESRS standards, conducting formal double materiality assessments, and establishing data systems that meet audit requirements. It is essential for manufacturing and construction companies to integrate continuous data governance, early software adoption, and stakeholder engagement to ensure compliance and avoid common pitfalls. Building internal capacity, applying automated XBRL tagging, and treating sustainability reporting as an ongoing process are critical for successful CSRD compliance.

Aligning with EU sustainability standards means mastering the European Sustainability Reporting Standards (ESRS) framework, completing a formal double materiality assessment, and building data systems that meet financial-grade audit requirements. For quality and sustainability managers in manufacturing and construction, knowing how to align with EU sustainability standards is no longer optional. The Corporate Sustainability Reporting Directive (CSRD) has been binding since 2024, and EFRAG developed ESRS as delegated regulation that supersedes earlier non-financial directives. This guide walks you through every critical step, from understanding the 12 ESRS standards to submitting a digitally tagged, assurance-ready report.

How to align with EU sustainability standards: the ESRS framework

The ESRS framework consists of 12 standards: 2 mandatory cross-cutting standards and 10 topical standards covering environment, social, and governance topics. That structure matters because it tells you exactly where to start and what you can deprioritize based on your materiality results.

ESRS 1 sets the general principles and architecture for all reporting. ESRS 2 requires general disclosures about governance, strategy, and materiality processes, and it applies to every company under CSRD without exception. The remaining 10 topical standards, covering areas like climate change (ESRS E1), biodiversity (ESRS E4), own workforce (ESRS S1), and business conduct (ESRS G1), only apply if your double materiality assessment confirms they are material to your business.

One important detail: climate change disclosures under ESRS E1 carry a rebuttable presumption of materiality. That means you must apply ESRS E1 unless you can formally document why climate change is not material to your operations. For manufacturers and construction companies, that argument is nearly impossible to make credibly.

EFRAG is also working to reduce the reporting burden. Revised drafts aim to cut data points by over 70%, with adoption expected in early 2026. That simplification is welcome, but it does not change the underlying compliance logic.

| Standard | Category | Scope |

|---|---|---|

| ESRS 1 | Cross-cutting | General principles, mandatory for all |

| ESRS 2 | Cross-cutting | Governance, strategy, materiality, mandatory for all |

| ESRS E1–E5 | Environmental | Climate, pollution, water, biodiversity, resource use |

| ESRS S1–S4 | Social | Own workforce, value chain workers, communities, consumers |

| ESRS G1 | Governance | Business conduct, anti-corruption |

How do you conduct a double materiality assessment?

Double materiality is the single biggest failure point in CSRD compliance. Companies that skip a formal assessment either over-report on irrelevant topics or under-report on material ones. Both outcomes create legal and reputational risk.

Double materiality combines two lenses. Financial materiality asks whether an ESG topic creates financial risks or opportunities for your company. Impact materiality asks whether your operations cause significant positive or negative impacts on people or the environment. A topic is material if it clears either threshold. A rigorous double materiality assessment ensures you focus only on what genuinely applies, avoiding the waste of applying all ESRS standards indiscriminately.

The formal process follows four steps:

- Define organizational context. Map your value chain, business model, and key relationships. For a construction company, this includes subcontractors, material suppliers, and site operations across multiple geographies.

- Identify potential impacts, risks, and opportunities. Use your value chain map to list ESG topics that could be material. Involve procurement, operations, finance, and legal teams at this stage.

- Assess severity and likelihood. Score each topic by the scale, scope, and irremediability of its impact, and by the probability and magnitude of financial effects.

- Document and validate. Record your methodology, scoring rationale, and stakeholder inputs. This documentation becomes part of your ESRS 2 disclosures and will be reviewed by your assurance provider.

Pro Tip: Engage cross-functional teams before you start scoring. Procurement managers often hold the most accurate data on Scope 3 emissions and supply chain risks. Sustainability managers who run this process alone consistently miss material topics that sit outside their direct visibility.

You can find a detailed methodology in this step-by-step materiality guide that covers both financial and impact dimensions with practical examples.

What internal systems does ESRS reporting actually require?

CSRD requires internal controls for sustainability data that mirror the rigor applied to financial reporting. That is a significant shift for most manufacturing and construction companies, where ESG data has historically lived in spreadsheets owned by one person.

You need documented data collection processes with clear ownership, defined data sources, and audit trails for every metric. Scope 1 and Scope 2 emissions are relatively straightforward to collect. Scope 3 is where most companies struggle. Building automated data pipelines for supplier emissions, logistics, and product end-of-life requires coordination across procurement, logistics, and product development teams.

The digital compliance requirement adds another layer. XBRL tagging and the European Single Electronic Format (ESEF) are legally required for CSRD filings. Your sustainability report must be machine-readable, not just a PDF. This is not a formatting preference. It is a legal requirement.

When evaluating ESG software platforms, look for these features:

- Native XBRL tagging mapped to ESRS disclosure requirements

- Automated data validation that flags missing or inconsistent entries before submission

- Multi-entity consolidation for companies with subsidiaries or joint ventures

- Audit trail functionality that records who entered data, when, and from what source

- Structured workflows that assign data collection tasks to specific owners across departments

Pro Tip: Select and implement your ESG software platform at least 12 months before your first reporting deadline. Companies that wait until the final quarter face two problems: rushed implementation with poor data quality, and last-minute manual XBRL tagging that is expensive and error-prone.

Selecting ESG reporting software with native XBRL and audit features early is one of the highest-leverage decisions you will make in this process.

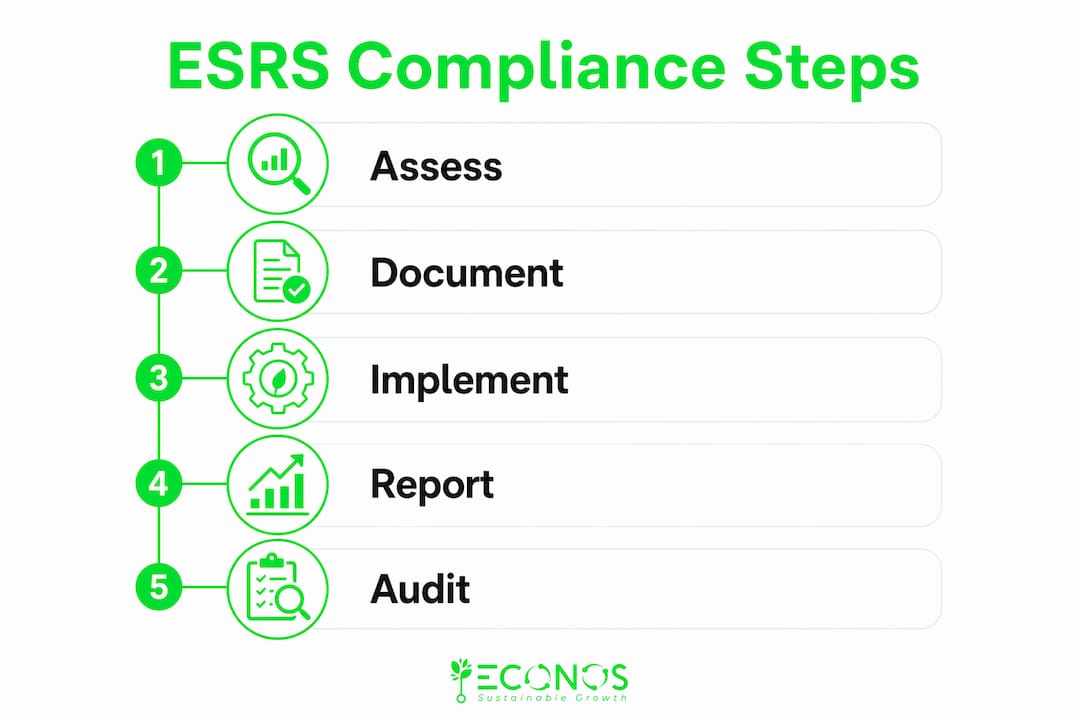

What are the steps to submit a compliant sustainability report?

Preparing and submitting a compliant CSRD report is a structured process with clear milestones. Engaging assurance providers early is one of the most consistently overlooked steps, and it is one of the most consequential.

Follow this sequence to stay on track:

- Perform a gap analysis. Compare your current ESG data collection practices against every disclosure requirement in your material ESRS standards. Document what you have, what you are missing, and what requires a new data source.

- Build your data infrastructure. Assign ownership for each data point. Establish collection processes, validation rules, and storage systems that meet audit requirements.

- Integrate sustainability disclosures into your management report. CSRD requires sustainability information to appear within the management report, not as a standalone document. Coordinate with your finance team early.

- Engage your assurance provider. Limited assurance is required for the first reporting cycle. Your auditor needs time to understand your data processes, test controls, and raise questions before the report is finalized.

- Consolidate multi-entity data. For manufacturing groups with multiple legal entities or construction companies operating across countries, consolidation requires clear reporting boundaries and consistent methodologies.

- Apply XBRL tags and finalize the digital filing. Do not leave this step for the last week. Manual tagging errors are common and can delay submission.

- Communicate with stakeholders. Investors, customers, and procurement teams will read your report. Plan how you will present material findings and what follow-up questions you expect.

A practical sustainability reporting checklist can help you track progress against each of these milestones throughout the year.

What are the most common pitfalls in EU sustainability compliance?

Treating sustainability reporting as annual paperwork rather than a continuous business process is the root cause of most compliance failures. Companies that operate this way are always behind, always scrambling, and always producing lower-quality disclosures.

The five most common pitfalls, and how to avoid them:

- Misapplying double materiality. Applying all ESRS standards without a formal assessment wastes resources and produces disclosures that lack credibility. Conduct the assessment first, document it thoroughly, and let it drive your reporting scope.

- Understaffing the function. One sustainability manager cannot own CSRD compliance alone. The data collection burden spans procurement, HR, finance, legal, and operations. Build a cross-functional team with clear accountability.

- Delaying software selection. Companies that choose ESG platforms late in the cycle face rushed implementation and poor data quality. Start the selection process at least a year before your first deadline.

- Ignoring Scope 3 until it is too late. Scope 3 emissions typically represent the largest share of a manufacturer’s carbon footprint. Collecting supplier data takes time. Start supplier engagement 18 months before your first report.

- Last-minute XBRL tagging. Manual tagging at the end of the process is expensive and error-prone. Choose a platform with automated XBRL support from the start.

“Double materiality is not a checkbox. It is a legal determination that defines your compliance scope. Getting it wrong means your report is either incomplete or misleading. Neither outcome is acceptable under CSRD.”

Key takeaways

Successful alignment with EU sustainability standards requires a formal double materiality assessment, financial-grade data governance, and early adoption of XBRL-ready reporting systems.

| Point | Details |

|---|---|

| Start with double materiality | Conduct a formal four-step assessment before selecting which ESRS standards apply to your organization. |

| ESRS 1 and ESRS 2 are always mandatory | Every CSRD-reporting company must comply with both cross-cutting standards, regardless of materiality results. |

| Build data systems early | Establish documented data pipelines and ownership structures at least 12 months before your first reporting deadline. |

| XBRL tagging is a legal requirement | ESEF digital format is mandatory for CSRD filings. Choose software with native tagging support from the start. |

| Treat reporting as a continuous process | Annual document creation fails. Compliance requires year-round data collection, governance, and stakeholder engagement. |

What i have learned working on CSRD readiness in manufacturing

The gap I see most often is not a lack of ambition. It is a lack of data governance. Companies in manufacturing and construction have the will to comply, but their ESG data is scattered across departments with no clear ownership and no audit trail. That is not a sustainability problem. It is a management problem, and it needs a management solution.

The companies that get this right treat their sustainability data with the same rigor they apply to financial data. They assign owners, document sources, validate entries, and build review cycles into their calendar. The ones that struggle treat CSRD as a reporting exercise rather than a governance transformation.

I also want to be honest about the regulatory environment. The EU is actively revising ESRS to reduce the data point burden, and the timeline for smaller companies continues to shift. That creates real uncertainty. My advice is to build your foundation on the mandatory requirements (ESRS 1, ESRS 2, and your material topical standards) and avoid over-investing in disclosures that may be simplified or removed. Flexibility matters as much as thoroughness right now.

The technology piece is underrated. Companies that adopt purpose-built platforms early move faster, produce cleaner data, and spend less on assurance fees. The greening process is not just about what you report. It is about how you build the internal capacity to keep reporting accurately, year after year.

— Mathieu

How Econos-esg helps you get compliant and stay ahead

Econos-esg works with manufacturers and construction companies at every stage of CSRD alignment, from initial gap analysis through assurance-ready report submission. The team brings hands-on experience across carbon footprint assessment (Scope 1, 2, and 3), ESRS reporting, EU Taxonomy classification, and CBAM compliance.

For companies starting their compliance process, Econos-esg’s carbon footprint assessment service builds the emissions data foundation that ESRS E1 requires. For companies further along, the ESG reporting service covers full CSRD disclosure preparation, XBRL tagging support, and assurance readiness. Econos-esg’s training-first model means your team builds real internal capacity, not dependency on external consultants. Reach out to discuss where your organization stands and what the next step looks like.

FAQ

What is the CSRD and who does it apply to?

The Corporate Sustainability Reporting Directive (CSRD) is EU law requiring large companies and listed SMEs to report sustainability information under ESRS standards. It applies to companies meeting two of three thresholds: over 250 employees, over €40 million in turnover, or over €20 million in total assets.

What is double materiality under ESRS?

Double materiality requires companies to assess both financial materiality (ESG risks and opportunities affecting the company) and impact materiality (the company’s effects on people and the environment). A topic is material if it clears either threshold, and the assessment must be formally documented.

Which ESRS standards are mandatory for all companies?

ESRS 1 and ESRS 2 are mandatory for every company reporting under CSRD, regardless of sector or materiality results. All other topical standards apply only if confirmed material through a formal double materiality assessment.

What is XBRL tagging and why does it matter?

XBRL tagging is the process of marking up sustainability disclosures in a machine-readable format required by the European Single Electronic Format (ESEF). It is legally required for CSRD filings and must be applied to the full sustainability report before submission.

How early should we start preparing for CSRD compliance?

Start at least 18–24 months before your first reporting deadline. Gap analysis, software selection, data pipeline construction, and assurance provider engagement all require significant lead time, particularly for Scope 3 emissions data collection across your supply chain.