.png)

TL;DR:

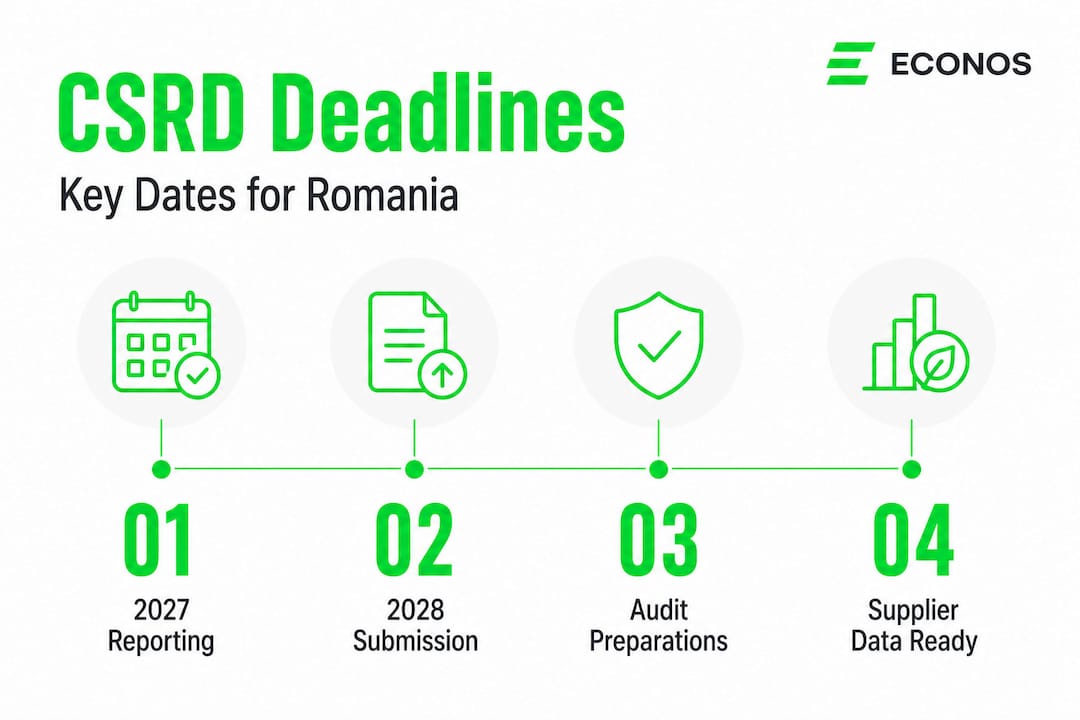

- Romanian companies have until 2027 and 2028 to prepare for CSRD reporting obligations.

- Building internal ESG capabilities and data systems now is crucial despite the deadline extension.

- Automated carbon management enhances data accuracy, efficiency, and audit readiness for sustainability reporting.

Romania’s sustainability reporting landscape shifted dramatically in 2025, and many companies are still sorting out what it actually means for them. Order No. 1421/2025 postponed CSRD deadlines by two years for most in-scope Romanian businesses, triggering a wave of relief in boardrooms across the country. But here is the uncomfortable truth: relief about a deadline is not the same as readiness. The companies that treat this extension as permission to pause are making a costly mistake, and sustainable management consulting is one of the clearest ways to avoid it.

Table of Contents

- CSRD and ESG: What Romanian companies must know now

- Building capacity for sustainability: From gap analysis to audit-readiness

- Value-chain data and supplier engagement: A Romanian perspective

- Automated carbon management: Integrating data for real ESG impact

- The real lessons Romanian companies should learn from Europe’s sustainability push

- How ECONOS empowers sustainable management for Romanian companies

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| CSRD deadlines postponed | Romanian companies report CSRD-aligned data for 2027 and 2028, but should act now on readiness. |

| Capacity building is essential | Consulting support for materiality, gap analysis, and audit-readiness lays the foundation for compliance. |

| Supplier data is critical | Value-chain engagement is necessary to meet CSRD data requirements, not just facility data. |

| Automation accelerates compliance | Digital carbon management tools streamline ESG data integration and reporting. |

| Early action pays off | Companies prepared ahead of the deadline avoid last-minute risks and capture ESG opportunities. |

CSRD and ESG: What Romanian companies must know now

The Corporate Sustainability Reporting Directive, known as CSRD, is the European Union’s framework requiring companies to disclose detailed environmental, social, and governance (ESG) information according to a set of standards called ESRS (European Sustainability Reporting Standards). For Romanian companies, the practical question has always been: when, and who?

Following the new government order, CSRD compliance deadlines for medium and large Romanian companies have been moved to financial years 2027 and 2028. Here is what that looks like in practice:

| Company type | Reporting for financial year | First report due |

|---|---|---|

| Large companies (public interest) | 2025 | 2026 |

| Large companies (other) | 2027 | 2028 |

| Medium companies | 2028 | 2029 |

| Listed SMEs (voluntary) | 2028 | 2029 |

The good news is that most Romanian mid-sized and large companies now have more runway. The hard truth is that this runway has to be used productively. Understand the full scope of CSRD requirements before deciding how to use that time.

What should companies do during this “stop-the-clock” period? Quite a lot, actually:

- Identify your reporting perimeter. Which entities and subsidiaries fall under CSRD? This is not always obvious for complex corporate structures.

- Assess your current data maturity. Can you measure your Scope 1 and Scope 2 carbon emissions accurately? What about Scope 3 (value chain emissions)?

- Map your stakeholders. ESRS requires structured stakeholder engagement as input to your materiality assessment.

- Design internal governance. Who owns ESG data? Who is accountable for reporting accuracy? These roles need to exist before reporting starts.

- Begin your double materiality assessment. This is a non-trivial, structured process that takes months to do well.

A reporting checklist for compliance can help structure these early steps and identify gaps before they become urgent problems.

The delay does not postpone infrastructure requirements. Auditors will eventually assess the quality and traceability of your data, not just the numbers you report. Companies that start building systems in 2026 will look very different from those that start in 2027 under time pressure.

Building capacity for sustainability: From gap analysis to audit-readiness

One of the most important concepts in CSRD is double materiality. It sounds technical, but it has a straightforward meaning in practice. Romanian firms must analyze sustainability topics from two directions: how the company’s activities impact the environment and society (impact materiality), and how environmental and social issues create financial risks or opportunities for the company (financial materiality). Double materiality is a central concept for CSRD and ESRS compliance, not a checkbox to tick but a genuine analytical process.

Many companies underestimate how much structured work this involves. A consulting-supported process typically follows these steps:

- Topic mapping. Identify all potential sustainability topics relevant to your industry, geography, and business model. ESRS provides a starting list, but it needs to be filtered and adapted to your context.

- Stakeholder identification and engagement. Map internal and external stakeholders (employees, customers, suppliers, communities, regulators) and gather their perspectives on material topics. This requires structured surveys, interviews, or workshops.

- Impact and risk analysis. For each topic, assess the severity and likelihood of impacts, and evaluate the financial materiality of related risks and opportunities. This is where solid data and honest judgment matter most.

- Materiality validation. Present findings to senior leadership and the board for validation. ESG governance is not a sustainability team task; it requires executive ownership.

- ESRS matrix construction. Based on validated materiality results, determine which ESRS disclosure requirements apply to your company and build your reporting architecture accordingly.

“Sustainability reporting is not a documentation exercise. It is a decision-making framework. The companies that treat it as paperwork will never get the strategic value out of it.”

Documentation and audit-readiness must be built into the process from the start. Every step should generate evidence: meeting records, stakeholder responses, scoring rationale, and governance approvals. When external assurance becomes mandatory, auditors will ask for this trail.

Pro Tip: Start your double materiality assessment at least 18 months before your first reporting deadline. The consultation and validation cycles alone can take six months, and you will need the rest of the time to fill data gaps identified during the process. Use a sustainability reporting checklist to track progress across every workstream.

A detailed ESG reporting guide can help companies understand what “audit-ready” actually looks like and what documentation is needed to get there.

Value-chain data and supplier engagement: A Romanian perspective

Internal data is hard enough to collect. Value-chain data is where most Romanian companies hit a wall. ESRS S2 (workers in the value chain), E1 (climate), and other standards require companies to go beyond their own operations and gather information from suppliers, customers, and other value-chain partners.

CSRD-aligned reporting requires information beyond entity operations, meaning consultants increasingly focus on supplier engagement and systematic data collection workflows. Here is how internal reporting and value-chain reporting compare:

| Dimension | Internal reporting | Value-chain reporting |

|---|---|---|

| Data scope | Company-owned operations | Suppliers, logistics, customers |

| Data availability | Generally higher | Often incomplete or estimated |

| Control level | High | Low to medium |

| Consulting focus | Systems and governance | Supplier programs and capacity |

| Key challenge | Data quality | Data collection and response rates |

Consultants help companies design supplier data-collection programs that are realistic and proportionate. This means identifying which suppliers matter most (by spend, emission intensity, or impact category), developing supplier questionnaires aligned to ESRS and EcoVadis frameworks, and building a communication cadence that actually gets responses.

- Prioritize by materiality. Not every supplier needs to be surveyed. Focus first on the top 20% by spend or the highest-impact categories.

- Use standardized templates. Suppliers are often being asked for sustainability data by multiple customers. Aligned formats reduce friction and improve response rates.

- Document your efforts. If a supplier does not respond, ESRS allows for documented estimation under certain conditions. The documentation of your outreach is itself audit evidence.

- Build supplier relationships. Engagement works better as a collaborative process than as a compliance demand. Offering capacity-building support to key suppliers creates goodwill and better data.

Pro Tip: Begin your supplier engagement program at least one full year before your reporting deadline. Supplier response cycles are slow, and first-year data is almost always incomplete. Planning for iteration is not a failure; it is good practice. A sustainable procurement guide can help structure a procurement strategy that supports your CSRD data needs systematically.

Missing supplier data is not a reporting failure if it is handled transparently. What is a failure is discovering the gap six weeks before your report is due.

Automated carbon management: Integrating data for real ESG impact

Carbon footprint measurement sits at the heart of CSRD compliance. Climate-related disclosures under ESRS E1 require companies to report Scope 1, Scope 2, and Scope 3 greenhouse gas emissions, along with targets, transition plans, and scenario analysis. Doing this manually, through spreadsheets and fragmented data sources, is not sustainable at scale.

Automated carbon management refers to the use of software platforms and structured workflows that pull activity data from business systems (ERP, procurement, HR, logistics), apply recognized emission factors, and generate audit-ready carbon accounts. The benefits are concrete:

- Consistency. Automated systems apply the same methodology every period, reducing calculation errors and making year-on-year comparisons meaningful.

- Efficiency. Finance and sustainability teams spend less time hunting for data and more time interpreting it.

- Audit-readiness. Every data point can be traced to its source, which is exactly what assurance providers need.

- Scenario modeling. Good platforms let you test reduction scenarios against different business assumptions, which is critical for credible transition plans.

- Scope 3 coverage. Calculating value-chain emissions requires processing large volumes of supplier-level data. Automation makes this tractable.

Even with CSRD deadline relief, firms must set up governance, materiality processes, and robust data foundations early, as assurance requirements remain. This is where automated carbon management adds its most immediate value: it creates the data foundation that assurance providers will need, built progressively over time rather than assembled in a rush.

Consider a practical example. A mid-sized Romanian manufacturing company begins using an automated carbon management tool in early 2026. By mid-2027, they have two full years of consistent Scope 1 and Scope 2 data, a reliable Scope 3 methodology for their top emission categories, and documented data quality notes. When their first CSRD report is due, they are not scrambling. They are refining.

Companies can discover the broader business value from CSRD compliance when they treat carbon management as a strategic tool rather than a reporting obligation. Better energy data leads to better procurement decisions. Better supply chain visibility leads to lower operational risk.

The real lessons Romanian companies should learn from Europe’s sustainability push

We will be candid here. Having worked with companies like Michelin, Raiffeisen Bank, eMAG, and PORR across more than 158 projects in 17 industries, we have seen the same pattern repeat itself: companies wait for certainty before they act, and then certainty arrives in the form of a deadline they are not ready for.

The “stop-the-clock” extension is not a gift from regulators. It is a correction in timing, not in direction. Evidence quality and system readiness must start now, even when reporting is postponed. Europe’s sustainability push is not reversing. If anything, the standards will tighten as the European Commission develops sector-specific ESRS and extends CSRD coverage further.

The companies that delay capacity-building are not just postponing work. They are compressing it. Double materiality, supplier engagement, governance design, carbon measurement, and assurance preparation cannot all happen simultaneously in a six-month window. Organizations that try to do this under time pressure produce lower quality work, make more errors, and spend far more money than those who build steadily.

Here is the more important lesson, though. The real return on investment from sustainability consulting is not the report you produce. It is the internal capability you build. When your sustainability team understands why they are measuring what they are measuring, they make better decisions every day, not just at reporting time. When your procurement team knows how to evaluate suppliers on ESG criteria, they reduce risk continuously. When your leadership understands materiality, ESG becomes a strategic tool rather than a compliance cost.

Many companies confess to us that they initially hired consultants to “handle ESG” for them. That approach creates dependency and rarely builds the internal knowledge needed to sustain credible reporting over time. Our view, shaped by honest reflection on what actually works, is that unlocking value with CSRD requires building your team’s confidence and capability alongside the systems and reports. Compliance without understanding is fragile. Compliance with understanding is resilient.

How ECONOS empowers sustainable management for Romanian companies

At ECONOS, we built our consulting model around a simple belief: Romanian companies should not need us forever. From the first gap analysis through to your first audited sustainability report, our role is to transfer knowledge and capability, not to hold onto it.

Our ESG reporting services cover the full CSRD and ESRS journey, from double materiality assessments and stakeholder engagement to ESRS disclosure mapping and assurance preparation. Our carbon footprint assessment methodology covers Scope 1, 2, and 3, with AVA, our AI-powered carbon accounting assistant, helping your team collect data and run calculations autonomously. If you are ready to explore what a structured ESG readiness program looks like for your organization, visit our sustainability consulting solutions page and let’s start an honest conversation about where you are and where you need to be.

Frequently asked questions

What is the current CSRD reporting deadline for Romanian companies?

Romanian medium and large companies must report CSRD-aligned information for financial years 2027 (report due 2028) and 2028 (report due 2029), following the new government order.

Does the deadline extension allow companies to delay ESG system readiness?

No. Companies still need to build governance, reporting, and data systems now, because assurance and evidence quality standards remain in place regardless of when the first report is due.

What does double materiality mean for Romanian companies?

Double materiality requires companies to analyze both how their business affects sustainability topics (impact materiality) and how sustainability issues create financial risks or opportunities for the company (financial materiality).

How can consultants help with missing value-chain data?

Consultants design supplier engagement processes and workflows so companies can document their data-collection efforts systematically, making consistent progress and meeting assurance expectations even when some supplier data is incomplete.

What is the main benefit of automated carbon management for ESG reporting?

Automated carbon management significantly boosts reporting reliability and audit-readiness by ensuring consistent methodology and traceable data across every reporting period, while also reducing the manual workload on sustainability and finance teams.