.png)

TL;DR:

- Many Romanian companies treat CSRD compliance as a checkbox, missing its potential strategic value.

- CSRD requires comprehensive, digitally tagged, forward-looking sustainability disclosures based on double materiality.

- Proactive integration of CSRD can enhance risk management, investor trust, and supply chain resilience.

Most companies in Romania and neighboring countries still treat CSRD as a compliance checkbox: something to survive, not leverage. That instinct is understandable, but it is also costly. The Corporate Sustainability Reporting Directive is not just a reporting upgrade. It is a structural shift in how businesses account for their impact on the world and how the world accounts for risk in them. Companies that grasp this early will not just avoid penalties. They will attract better investors, build stronger supply chains, and earn genuine stakeholder trust. This article breaks down what CSRD actually requires, how it applies regionally, and how to turn it into a real business advantage.

Table of Contents

- What is the CSRD and why it matters for your business

- Double materiality and stakeholder engagement: A new lens for sustainability

- Navigating regional CSRD rollout: Romania and neighboring countries

- From compliance to value creation: How CSRD drives sustainable strategy

- A fresh perspective: The real ROI of CSRD beyond compliance

- Next steps: Get support for your CSRD journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| CSRD changes reporting | CSRD forces companies to elevate sustainability from compliance to strategic advantage. |

| Double materiality clarified | CSRD uses double materiality so firms report impacts on both society and financial value. |

| Regional rollout matters | Romanian and neighboring companies face phased deadlines and thresholds, requiring prepared action. |

| Value creation is possible | CSRD lets companies go beyond paperwork, building trust and resilience in the market. |

| Expert support available | Specialized consulting and platforms can simplify CSRD and help unlock true ESG value. |

What is the CSRD and why it matters for your business

The Corporate Sustainability Reporting Directive replaced the older Non-Financial Reporting Directive (NFRD) and raised the bar significantly. Where NFRD was vague and largely voluntary in practice, CSRD is specific, mandatory, and externally assured. It requires companies to report sustainability information under the European Sustainability Reporting Standards (ESRS), covering everything from climate and biodiversity to social conditions and governance.

What makes CSRD structurally different is its reach. Reporting covers own operations plus upstream and downstream value chain, and it requires digital XHTML tagging, limited assurance from an auditor, and forward-looking information. This is not a summary of past performance. It is a living document of where your business is headed and what risks and impacts it carries.

For companies operating in Romania, Bulgaria, and Hungary, CSRD implementation is already underway. The directive has been transposed into national law, and reporting timelines are active. Understanding ESG reporting requirements early gives your team time to build systems rather than scramble.

Here is what CSRD requires at a glance:

- Digital reporting: Sustainability data must be tagged in XHTML format for machine readability

- Value chain coverage: You must account for Scope 3 emissions and social impacts across suppliers and customers

- Limited assurance: An independent auditor must verify your disclosures

- Forward-looking targets: You need to show where you are going, not just where you have been

- Double materiality assessment: More on this below, but it is central to everything

Strategically, CSRD gives companies a structured reason to understand their carbon footprint and supply chain risks. That knowledge is genuinely valuable, not just for reporting, but for procurement decisions, investor conversations, and operational resilience.

Pro Tip: Start with a gap analysis before anything else. Map what data you currently collect against what CSRD requires. This single step will save months of confusion and help you prioritize where to invest time and resources first.

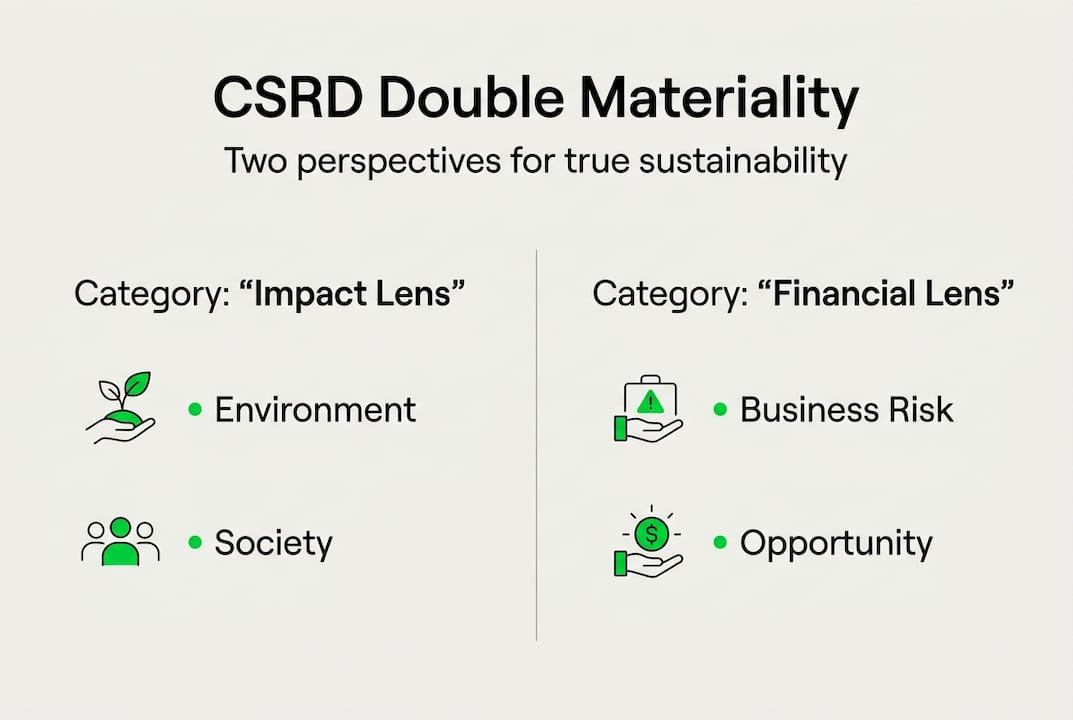

Double materiality and stakeholder engagement: A new lens for sustainability

If there is one concept that separates CSRD from every previous reporting framework, it is double materiality. Most companies are familiar with financial materiality: what matters to investors. CSRD adds a second dimension.

Double materiality requires assessing impacts on environment and society (evaluated by severity: scale, scope, and irremediability) OR financial effects on enterprise value (evaluated by likelihood and magnitude). The key word is “OR.” You do not need both dimensions to trigger a disclosure obligation. Either one is enough.

This changes how companies think about risk. A factory that pollutes a local river may not face immediate financial loss, but the impact on the environment is material under CSRD. Conversely, a supplier dependency that could disrupt revenue is financially material even if it has no direct environmental consequence.

Here is how CSRD’s double materiality compares to older approaches:

| Dimension | Previous NFRD approach | CSRD double materiality |

|---|---|---|

| Focus | Primarily financial risk | Financial AND environmental/social impact |

| Stakeholder scope | Investors | Investors, communities, employees, supply chain |

| Assurance required | Voluntary | Limited assurance mandatory |

| Value chain coverage | Own operations | Full upstream and downstream |

Stakeholder engagement is not optional under CSRD. It must be iterative and proportionate, meaning you revisit it as your business evolves. LCA methodology can support this by quantifying environmental impacts across the product lifecycle, giving your materiality assessment a factual backbone.

A practical approach to stakeholder engagement involves these steps:

- Map all relevant stakeholders: employees, suppliers, local communities, investors, regulators

- Conduct structured interviews or surveys to identify their sustainability concerns

- Cross-reference their inputs with your operational data to identify overlap

- Prioritize topics by severity and financial relevance

- Document the process transparently for your auditor

“The double materiality assessment is not a one-time exercise. It is a living process that should evolve as your business, your supply chain, and your stakeholder expectations change. Companies that treat it as a checkbox will find themselves revisiting it under pressure.” Edge cases and relief mechanisms confirm that even subsidiaries face entity-specific disclosure requirements in certain situations.

For ESG and materiality practitioners, the message is clear: build a process, not just a document.

Navigating regional CSRD rollout: Romania and neighboring countries

With double materiality understood, the practical question becomes: when does this apply to your company, and what does it look like in your country?

In Romania, approximately 5,300 companies meeting at least two of three thresholds (RON 25M in assets, RON 50M in turnover, or 50+ employees) must report, with phased timelines starting from 2024 and 2025. The challenges are real: data gaps, limited internal expertise, and training needs are the most commonly cited barriers.

Neighboring countries have followed similar paths. Bulgaria delayed its reporting requirements by one year. Hungary passed its ESG Act in 2023, with thresholds set at 250 employees or HUF 20 billion in turnover. All countries are implementing phased timelines, but the underlying standards remain consistent.

| Country | Key threshold | Reporting start | Notable feature |

|---|---|---|---|

| Romania | RON 25M assets / RON 50M turnover / 50+ emp | 2024/2025 (phased) | ~5,300 companies in scope |

| Bulgaria | Similar EU thresholds | Delayed by 1 year | National act transposed |

| Hungary | 250 emp / HUF 20B turnover | 2025 (phased) | ESG Act 2023 |

For Romanian companies specifically, the pressure is compounding. Large enterprises in scope since 2024 are already reporting, while mid-sized companies entering scope in 2025 and 2026 are still building their systems.

Practical considerations for companies in the region:

- Data collection: Many companies lack systems to track Scope 3 emissions or social metrics across their supply chain

- Internal capacity: Sustainability reporting requires cross-functional involvement, not just a single ESG manager

- SME relief mechanisms: Proportionality provisions exist, but they do not eliminate the obligation entirely

- Subsidiary exemptions: If your parent company reports at group level, you may qualify for exemption, but verify this with your auditor

- Training investment: Regulatory knowledge gaps are the most common reason companies fall behind schedule

The honest reality is that most mid-sized companies in the region are behind. Not because they lack commitment, but because the requirements are genuinely complex and resources are limited.

From compliance to value creation: How CSRD drives sustainable strategy

The 2025 Omnibus package introduced significant changes. The revised scope now covers companies with over 1,000 employees and €450M in turnover, reducing the number of affected companies by roughly 90%. ESRS datapoints were simplified. But double materiality remains intact, and here is the part most companies miss: banks and investors are still demanding this data regardless of whether you are legally required to report it.

That changes the calculus entirely. Even if your company falls outside the revised scope, your customers and financiers may still require CSRD-aligned disclosures. Voluntary alignment is no longer just good practice. It is a market positioning decision.

The strategic advantages of treating CSRD as a business tool rather than a burden include:

- Risk reduction: Identifying environmental and social risks before they become financial ones

- Supply chain resilience: Understanding your value chain deeply enough to anticipate disruptions

- Investor trust: ESG-aligned companies attract longer-term, lower-cost capital

- Innovation driver: Sustainability constraints often reveal operational efficiencies and new product opportunities

- Competitive differentiation: In procurement processes, especially for EU-funded projects, ESG credentials matter

Pro Tip: Align your CSRD reporting with GRI or ISSB standards where possible. Many of the data points overlap, and cross-referencing frameworks reduces duplication of effort while strengthening your credibility with international stakeholders.

For ESG best practices that go beyond minimum compliance, the companies we see succeeding are those that connect sustainability metrics to operational KPIs. They are not reporting for auditors. They are managing with the data. SME-specific reporting guidance is also available for companies that want to align voluntarily without the full ESRS burden.

The CSRD preparation landscape in Romania shows a split: larger companies are investing in digital tools and cross-functional task forces, while smaller ones are still trying to understand the basics. The gap is widening. The Omnibus debate has not resolved the underlying tension between regulatory burden and voluntary advantage. But the market signal is clear.

A fresh perspective: The real ROI of CSRD beyond compliance

Here is an uncomfortable truth we have observed across more than 158 projects: the companies that treat CSRD as a documentation exercise will spend significant resources and gain almost nothing. The companies that treat it as a mirror, something that forces them to look honestly at their operations, their supply chains, and their stakeholder relationships, will come out of this process fundamentally stronger.

The real return on investment in CSRD is not a cleaner audit. It is organizational clarity. When your teams understand why your carbon footprint matters, why your suppliers’ labor conditions are your business, and why your investors are asking different questions, something shifts. Sustainability stops being a department and starts being a lens.

Most companies miss this because they outsource the thinking. They get a report, but not the understanding. At ECONOS, we have built our entire model around the opposite approach: building internal capacity so your team owns the process. Explore case studies and success stories from companies that made this shift. The pattern is consistent: those who invest in understanding outperform those who invest only in reporting.

Next steps: Get support for your CSRD journey

CSRD compliance is genuinely complex, but it does not have to be overwhelming. The right support makes the difference between scrambling at deadline and building a system that works for you year after year.

At ECONOS, we help mid-sized and large companies across Romania and the region navigate ESG reporting with clarity and confidence. Whether you need EcoVadis certification support to strengthen your supply chain positioning, or LCA services to build a credible environmental baseline, our team brings both technical expertise and a training-first mindset. We do not just deliver reports. We build your internal capability so you stay in control. Reach out to explore how we can support your CSRD readiness today.

Frequently asked questions

Which companies in Romania need to comply with CSRD?

CSRD applies to approximately 5,300 Romanian companies meeting at least two of three thresholds: RON 25M in assets, RON 50M in turnover, or 50 or more employees, with phased reporting starting in 2024 and 2025.

What is double materiality under CSRD?

Double materiality means assessing both your company’s impacts on the environment and society and the financial effects of sustainability risks on your enterprise value, using an “OR” logic to determine what requires disclosure.

Are subsidiaries exempt from CSRD reporting?

Subsidiaries may be exempt if their parent company consolidates sustainability reporting at group level, but entity-specific circumstances can still trigger disclosure requirements, so verify your status carefully.

How can companies turn CSRD compliance into business value?

By aligning sustainability reporting with strategic goals, using gap analysis, cross-functional task forces, and digital tools, companies can improve risk management, strengthen investor relationships, and build a more resilient market position.